Understanding Cashflow in a Business

Understanding your Financial Statements – Part 5

Your business needs profits to grow and to provide a return on your investment. But profits cannot be used until they become cash. When businesses fail, they are often profitable but still run out of cash, unable to pay their bills.

Cash flow management is as important as profitability therefore, understanding cashflow in a business is essential.

In this article we’ll discuss:

- Introduction – Balance Sheet recap

- Measuring Your Cashflow

- Cashflow for Growing Businesses

Introduction

Lets start with a quick Balance Sheet recap

The third article in this series discussed reading a balance sheet. In summary, the balance sheet contains three types of values:

Assets:

Assets are items of value owned by the business, such as equipment and money in the bank. Assets will bring future financial benefits to the business.

Liabilities:

Liabilities are items owed by the business, such as amounts owed to suppliers (creditors) and bank loans. Liabilities will cause future financial outflows from the business.

Equity:

Equity is the surplus of assets over liabilities and represents the net worth of the business to the owner(s).

We can break both assets and liabilities into current and non-current, with current being due within one year and non-current being due after a year. E.g., if you have a bank loan with a five-year term, the portion payable within the next year will be included in your balance sheet under current liabilities while the remainder, due during years 2 – 5, will be shown separately under non-current liabilities.

To manage our short-term cash flow, we focus on the current items.

We want to know whether our current assets will cover our current liabilities. I.e., will we collect enough cash to pay our bills. This part of our balance sheet (current assets and liabilities) is known as our working capital.

A balance sheet normally lists current assets from most current down to least current. I.e., cash and money in the bank will be at the top, as they are immediately available. Debtors (money owed by clients) may be next, as they should be collected in cash within the next few weeks. Work in Progress (WIP) may be next, as it is work yet to be completed before it can be billed and eventually paid for.

Likewise, current liabilities due sooner will be listed above current liabilities due later.

Measuring Your Cash Flow

We will look at two ways to measure your business’s short-term financial health, or its ability to pay its bills as they become due: the working capital ratio and the cash conversion cycle.

1. Working Capital Ratio

Working capital ratio = current assets / current liabilities

The working capital ratio measures the ratio of current assets to current liabilities. I.e., the amount of current assets to come in for each dollar of current liabilities to go out. The higher the result, the better able the business is to pay its bills.

E.g., if your balance sheet shows total current assets of $30,000 and total current liabilities of $20,0000, you have a current ratio of 1.5 (30,000 / 20,000).

Whether 1.5 is good or not depends on the nature of your business. A consultant whose clients (or patients) have a consultation then pay before they leave, will not need as high a current ratio as a consultant who invoices their clients for payment on the 20th of the following month. The cash consultant knows they will collect money from cash sales over the following days and weeks in addition to the current assets in the balance sheet.

A variation of the working capital ratio is the quick ratio. The quick ratio excludes Work in Progress leaving just the most liquid, or readily convertible to cash, current assets. The quick ratio may be a better test of ability to pay bills if WIP will likely take some time to be completed.

Quick ratio = (current assets – WIP) / current liabilities

2. Cash Conversion Cycle (CCC)

CCC = WIP days + debtor days – creditor days

A second way to analyse your business’s cash flow, is by calculating the number of days it takes to generate cash. The cash conversion cycle (CCC) is slightly harder to calculate than the current or quick ratios, but may better explain the business’s ability to generate cash. Each of the three variables in the CCC equation above (WIP days, debtor days and creditor days) require separate calculations.

WIP days = WIP / direct costs x 365

WIP days measures how many days, on average, it takes for the business to complete work and get it invoiced, turning WIP in debtors. The fewer days, the more efficiently the business processes jobs once they have been started.

To calculate WIP days, take WIP from the balance sheet and divide it by the total expenses per the Profit and Loss. Multiply by 365 to convert it to the number of days.

Debtor days = debtors / fees (or sales) x 365

Debtor days measures how many days it takes to collect debtors. A low number of days indicates you have efficient trading terms and credit control. To calculate, use debtors from the balance sheet and fees from the profit and loss.

Creditor days = creditors / expenses x 365

Creditor days measure how long it takes you to pay your creditors. As you keep your money until you pay your creditors, a higher creditor days figure improves cash flow. It is generally considered good practice to delay paying creditors as long as you can without damaging your relations with your suppliers. Prompt payment discounts must also be weighed up.

To calculate, take creditors from the balance sheet and expenses from the profit and loss.

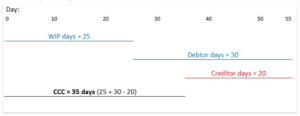

The following example shows a firm taking 25 days to complete jobs, 30 days to collect its debtors and 20 days to pay its bills. Its Cash Conversion Cycle is 35 days:

Cash flow for growing businesses

A business absorbs cash when it grows. Increased spending on staff, contractors and other expenses precede increased billing and cash collection. The longer the cash conversion cycle, the more money will be absorbed to grow the business.

When we hear that a failed business “grew too fast”, it really means they didn’t have the funding to grow that fast.

Good cash management, reducing the CCC days, limits the amount of growth cash required. However, there will usually still be shortfall which will have to be financed.

In the next article, we will look at long-term financing and how to ensure that a business has the resources to grow without running out of cash.

If you’re unsure about anything in this article and have more questions, feel free to get in touch.

Next Steps

Robb MacKinlay is an accountant and business advisor to professionals and consultants, helping them convert their expertise into profitable business.

Contact us with your business questions.

Did you find this article useful?

Please share this content using the social icons below and Sign Up to our mailing list to receive regular newsletters and information on relevant topics.