Residual, Provisional and Terminal Tax

What are they and when are they due?

If your tax bill is always a nasty surprise, read this! This article aims to demystify your income tax.

Once you understand how your tax is calculated and when it is due, you can plan for it. No more nasty surprises.

Everyone with business or other income that is not fully taxed at source must file a tax return and pay tax directly to IRD.

Below I explain the three tax payment terms you need to know:

If you’re unsure about anything in this article and have more questions, feel free to get in touch.

Residual Income Tax (RIT)

Your tax return contains your total taxable income from all sources.

Your tax payable on this income, after accounting for any tax already deducted at source (such as Resident Withholding Tax from interest or PAYE from wages), is your Residual Income Tax.

When and how this is paid to IRD is discussed below.

Provisional Tax

Once your Residual Income Tax (RIT) exceeds $2,500, you become a Provisional Tax payer from the following tax year. (Note: The government has increased the provisional tax threshold from $2,500 to $5,000 for the 2020-2021 income year due to the effects of covid 19).

You make Provisional Tax payments during a tax year towards that year’s RIT.

As you can’t calculate your final RIT until the year is finished, Provisional Tax is an estimate of your tax.

The default method for calculating Provisional Tax is adding 5% to the previous year’s RIT. Three other methods are available including estimating or basing it on your current year’s actual figures as you go.

Provisional Tax is usually paid in three instalments on 28 August, 15 January and 7 May. These dates assume you have a standard 31 March year end and, if you are GST registered, you file GST returns monthly or two-monthly.

If you file GST six-monthly, you have two Provisional Tax dates of 28 October and 7 May.

Presuming three Provisional Tax dates, for the tax year ending 31 March 2021, you pay Provisional Tax on:

- 28 August 2021

- 15 January 2022

- 7 May 2022

Terminal Tax

As the name suggests, Terminal Tax is the final tax payment for a year.

Terminal Tax is a year-end washup between Provisional Tax and Residual Income Tax.

- If you have not paid Provisional Tax, or your Residual Income Tax exceeds your Provisional Tax paid, the balance payable to IRD is your Terminal Tax.

- If your Provisional Tax exceeded your Residual Income Tax, your Terminal Tax is a refund from IRD.

Terminal Tax is due by 7 February following the tax year end, or 7 April if you have an extension of time, which you will generally have if you use an accountant.

For the tax year ending 31 March 2021, your Terminal Tax will be due 7 February 2022 or 7 April 2022. Again, these dates assume you have a 31 March year end.

Managing Your Income Tax

A simple business forecast will show you approximately what percentage of your earnings will go in tax.

By putting this percentage aside as the money comes in, you should always have your tax money available on the due dates.

Your first Provisional Tax date of 28 August is more than one third of the way through the financial year. Presuming your Provisional calculation is about right, by putting aside the money as you go, you should have more than a third of the year’s tax put aside by the time it is due.

Likewise, your second and third Provisional Tax dates, and your Terminal Tax date, all come after you have earned the money that you’re paying the tax on.

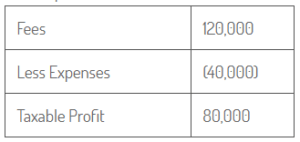

Income Tax Example

As a simple example, consider Tom, a consultant charging fees of $120,000 per year and business expenses of $40,000. His taxable profit is $80,000:

Tom’s Residual Income Tax on $80,000 works out to $17,320.

Tom calculates that approximately 14.4% of his fee revenue will go on tax (17,320 / 120,000). He puts aside 14.4% from every client payment.

By 31/7/21 (after 1/3 of the tax year) Tom has received $40,000 from clients and put $5,760 (40,000 x 14.4%) into a tax savings bank account. This should cover his provisional tax due on 28/8/21.

If your tax bill has taken you by surprise, there are ways to mitigate the damage including negotiating repayments with IRD or arranging tax finance.

However, understanding and planning for your tax obligations beats sorting out a mess at year-end.

Next Steps

Robb MacKinlay is an accountant and business advisor to professionals and consultants, helping them convert their expertise into profitable business.

Contact us with your business questions.

Did you find this article useful?

Please share this content using the social icons below and Sign Up to our mailing list to receive regular newsletters and information on relevant topics.